Taking out loans is one of the most common banking operations for everyday borrowers who need capital to invest or cover expenses they could not otherwise afford. These loans are not free: the price is the interest rate. Each bank in each country sets its own rate depending on the product—consumer credit, mortgages, housing loans, and so on.

Before applying for credit, it helps to understand the available payment structures so you do not fall behind and end up with negative reports in credit bureaus such as Datacrédito in Colombia.

The total cost of a loan depends heavily on the interest rate and on the payment schedule—for example, equal monthly installments versus variable installments tied to accrued interest, and whether an upfront payment is required.

In this post we show how to build a fixed-payment loan simulator in Python, which can be useful when comparing offers from financial institutions.

Building the simulator

First, install and import the required libraries. The main one is numpy_financial, which calculates the monthly installment; it can also compute interest rates and balances.

1

2

3

4

5

6

7

! pip install numpy_financial

import numpy as np

import pandas as pd

import numpy_financial as npf

import warnings

warnings.filterwarnings('ignore')

Next, define the simulator parameters: monthly interest rate, amount to finance, term in months (this simulator uses monthly frequency), and optional down payment.

1

2

3

4

tasa=0.0109

monto_financiar=500000

plazo=18

cuota_inicial=0

For this example we assume a 1.09% monthly rate, COP $500,000 financed over 18 months with no down payment—meaning each payment covers both principal and interest.

Then build a function that computes installments and returns an amortization table for each month. The function asks how many initial installments to pay; here we use 0 (the function handles loans with or without a down payment).

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

def cuota_fija(tasa,monto_financiar, plazo, cuota_inicial ):

base_liquidador=pd.DataFrame([])

cuota=npf.pmt(tasa, plazo,-monto_financiar, 0)

cuotas_iniciales=int(input("Enter value: "))

if cuotas_iniciales==1:

base_liquidador=pd.DataFrame([])

base_liquidador['Mes_cuota']=["Mes_%s"%(i+1) for i in range(plazo+1)]

base_liquidador['Saldo']=0

base_liquidador['Intereses']=0

base_liquidador['Saldo'][0]=monto_financiar

base_liquidador['Saldo'][1]=monto_financiar-cuota_inicial

base_liquidador['pago_mes']=int(cuota)

base_liquidador['pago_mes'][0]=cuota_inicial

base_liquidador['amortización']=0

base_liquidador['amortización'][0]=cuota_inicial

base_liquidador['tasa_interes']=tasa

base_liquidador['Saldo_final']=0

for i in range(0, len(base_liquidador)):

base_liquidador['Intereses'][i+1]=(base_liquidador['Saldo'][i]*base_liquidador['tasa_interes'][i])

base_liquidador['amortización'][i]=np.where(base_liquidador['Saldo'][i]>base_liquidador['Intereses'][i],(base_liquidador['pago_mes'][i]-base_liquidador['Intereses'][i]),base_liquidador['Saldo'][i] )

base_liquidador['Saldo'][i+1]=base_liquidador['Saldo'][i]-base_liquidador['amortización'][i]

base_liquidador['pago_mes'][i]=np.where(base_liquidador['Saldo'][i]>base_liquidador['amortización'][i], base_liquidador['pago_mes'][i], base_liquidador['Saldo'][i])

base_liquidador['Saldo_final'][i]=base_liquidador['Saldo'][i]-base_liquidador['amortización'][i]

elif cuotas_iniciales==0:

base_liquidador=pd.DataFrame([])

base_liquidador['Mes_cuota']=["Mes_%s"%(i+1) for i in range(plazo)]

base_liquidador['Saldo']=0

base_liquidador['Saldo'][0]=monto_financiar

base_liquidador['Intereses']=0

base_liquidador['pago_mes']=int(cuota)

base_liquidador['amortización']=0

base_liquidador['tasa_interes']=tasa

base_liquidador['Saldo_final']=0

for i in range(0, len(base_liquidador)):

base_liquidador['Intereses'][i]=(base_liquidador['Saldo'][i]*base_liquidador['tasa_interes'][i])

base_liquidador['amortización'][i]=np.where(base_liquidador['Saldo'][i]>base_liquidador['Intereses'][i],(base_liquidador['pago_mes'][i]-base_liquidador['Intereses'][i]),base_liquidador['Saldo'][i] )

base_liquidador['Saldo'][i+1]=base_liquidador['Saldo'][i]-base_liquidador['amortización'][i]

base_liquidador['Saldo_final'][i]=base_liquidador['Saldo'][i]-base_liquidador['amortización'][i]

else:

print("Oops! Invalid value. Try again...")

return base_liquidador

Run the function with the parameters defined above.

1

2

df=cuota_fija(tasa,monto_financiar, plazo, cuota_inicial )

print(df)

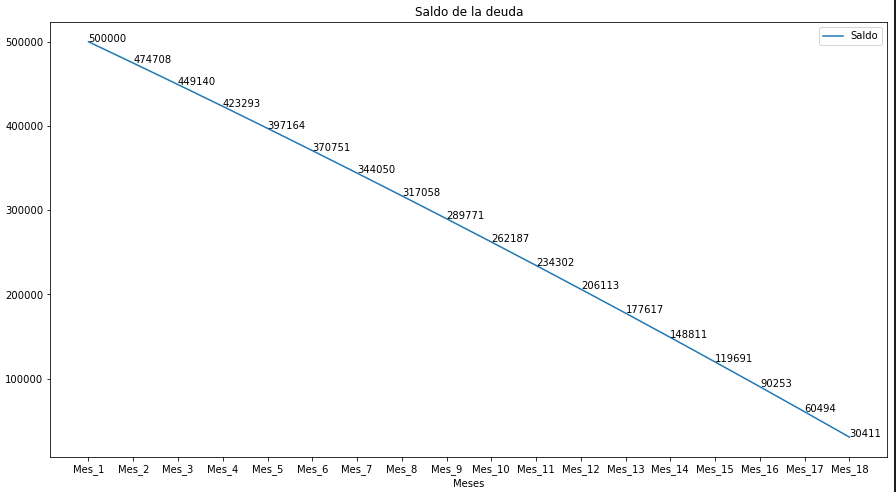

Amortization charts

The table below shows amortization behavior over the 18-month term.

The following code plots the outstanding principal balance.

1

2

3

4

5

6

7

8

9

10

import matplotlib.pyplot as plt

plt.figure(figsize=(15,8))

plt.plot(df.Mes_cuota,df.Saldo,label='Saldo')

plt.xlabel('Months')

plt.gcf().axes[0].yaxis.get_major_formatter().set_scientific(False)

plt.title('Outstanding balance')

for a,b in zip(df.Mes_cuota,df.Saldo):

plt.text(a, b, str(b))

plt.legend()

plt.show()

The chart below shows how the debt balance evolves across payment periods.

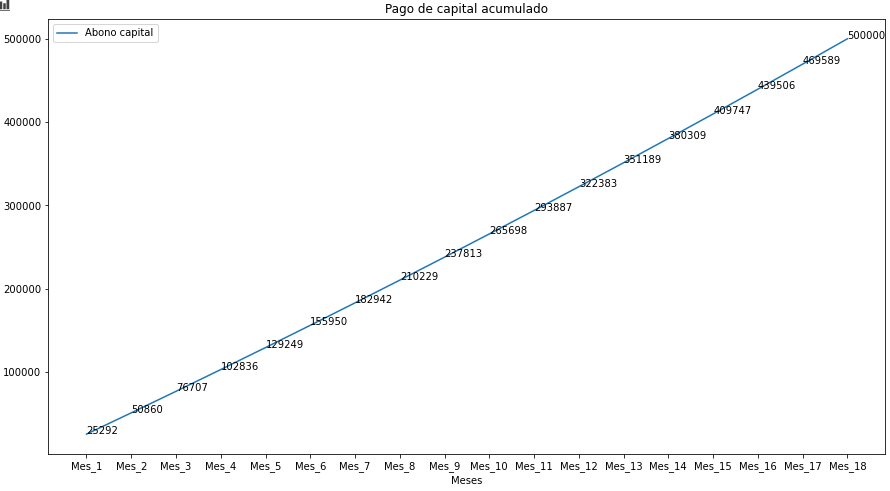

Finally, this code plots cumulative principal amortization for each period.

As Albert Einstein reportedly said, compound interest is the eighth wonder of the world: those who understand it benefit; those who do not pay it. As a reader exercise, try extending the simulator to variable-payment loans.